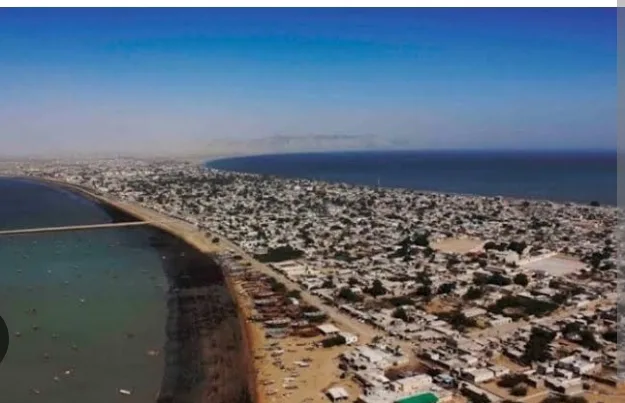

Pakistan is hard-selling Gwadar’s recent container numbers as a great achievement. One month in 2026 has already surpassed last year’s total container traffic, with approximately 11,000 containers processed in April, compared with roughly 8,300 for all of 2025. Pakistani authorities see this as a sign that long-promised investments are finally paying off. The bigger picture raises some deep questions — starting with the literal depth of the port itself.

In the world of container shipping, a few metres of water can mean the difference between a viable port and an expensive detour. Gwadar’s approach channel is currently maintained at approximately 12.5 metres — below its designed depth of 14 metres, due to the cost of dredging — and vessels with a draft of 13 to 14 metres, which are standard for major container services, cannot dock there. Officials credit the newly activated Iran road corridor and the Transit of Goods Order 2026 for the surge. What they discuss less readily is that the vessels calling at Gwadar are, by physical necessity, smaller and less efficient than those shaping global logistics at its most competitive level.

Neopanamax container ships, carrying between approximately 10,000 and 14,500 TEU, are the current workhorses of major Asia-Europe and transpacific trade lanes, and are built to a maximum draft of 15.2 metres. Beyond them, Ultra Large Container Vessels now operating on Asia-Europe routes carry over 24,000 TEU. Both classes are beyond what Gwadar can physically receive.

The vessels that can call at Gwadar are in the Panamax range — up to around 5,000 TEU with a draft of roughly 12 metres — a category that is increasingly being cascaded from mainline Asia-Europe and transpacific trade lanes onto secondary North-South routes as larger ships take over the primary trades. A port that cannot receive the industry’s dominant vessels cannot compete for the industry’s dominant trade flows.

The dredging mathematics compound the problem. Gwadar Bay experiences persistent siltation, meaning the seabed naturally rises over time. Maintaining the current 12.5-metre depth is not a one-time infrastructure investment but an ongoing operational cost requiring repeated dredging campaigns. Pakistan is currently supported by a $7 billion, 37-month IMF Extended Fund Facility, operating under strict fiscal targets including a primary surplus commitment, with total disbursements reaching approximately $3.3 billion by late 2025.

The fiscal pressure has already produced visible consequences at the port itself: Gwadar Port suffered a financial meltdown severe enough that it failed to pay employee salaries for November and December 2025. The prospect of funding far more expensive channel deepening work — and then sustaining the higher ongoing costs of maintaining a deeper channel against persistent siltation — has not been squarely addressed in any public plan.

The depth limitation was identified as a critical constraint years ago. Chinese investment in Pakistan under CPEC reportedly fell 74 percent in 2023 from the previous year, and the cumulative investment in Gwadar under the entire CPEC programme amounts to just $890 million — a tiny fraction of the corridor’s total portfolio.

Only two Chinese commercial firms have actually set up operations in Gwadar’s North Free Zone, and one of them — Hangeng Trade Company, a meat processor — has just shut its factory, citing an unworkable business environment and non-market barriers that left its export shipments stuck. This asymmetry — Chinese state involvement in port construction continuing alongside the near-absence of Chinese commercial shipping commitments — reflects a sophisticated distinction.

Chinese port operators, with extensive experience running deep-water facilities from Colombo to Hambantota, understand the economic gap between a 12.5-metre channel and a 15-metre one better than any promotional brochure acknowledges. Beijing wants Gwadar to work strategically. Chinese shipping companies need it to work on commercially rational terms.

The current traffic surge does not solve the depth problem; it may actually obscure it politically. The April container numbers are driven not by Gwadar’s improved competitiveness but by the US-Israeli war on Iran that began 28 February 2026, Iran’s closure of the Strait of Hormuz, and the US naval blockade of Iranian ports — a combination that forced cargo operators to seek overland alternatives and left more than 3,000 Iran-bound containers stranded at Karachi and Port Qasim until Pakistan activated its transit corridor on 25 April.

High container numbers create the impression of a thriving, competitive port even as the fundamental technical limitation remains unaddressed. For Pakistani officials who need to demonstrate CPEC progress to domestic audiences and to Beijing, the April figures provide useful cover. For the logistics planners at major shipping lines who will ultimately determine whether Gwadar becomes a serious regional hub, the channel depth is the first number they check — and at 12.5 metres, it closes the conversation before it begins.

The BLA’s maritime turn adds another layer of risk to this already challenging investment profile. In April 2026, the group conducted its first-ever sea operation near Jiwani, targeting a Pakistani Coast Guard patrol vessel, and simultaneously announced the formation of the Hammal Maritime Defence Force — signalling deliberate institutional investment in maritime operations rather than a one-off incident.

The insurance market has registered the broader regional shift: war-risk premiums for Gulf vessels rose from approximately 0.2 percent to as high as 1 percent of vessel value in the immediate aftermath of the conflict’s outbreak.

Claims of a “fortyfold surge” from 0.12% to nearly 5% that have circulated in some commentary are not supported by any documented source and should be disregarded. The actual figures are damaging enough: the emergence of a declared maritime insurgency in Gwadar’s own coastal waters can only add a distinct and unquantified local premium on top of already elevated regional rates.

The northern connectivity dimension that would make Gwadar genuinely transformative for China’s interior supply chains remains blocked at both ends. The ML-1 railway — the backbone of any serious northern corridor under CPEC — has stalled due to China’s concerns about Pakistan’s ability to service debt, and the last major CPEC infrastructure project completed was the Gwadar East Bay Expressway in 2022.

At the other end, Pakistan and Afghanistan are in a state of active armed conflict following Pakistan’s launch of Operation Ghazab lil-Haq in late February 2026, which involved airstrikes on Kabul, Kandahar, Paktia, and Nangarhar.

China-mediated talks in Urumqi in early April produced an agreement by both sides to work toward an early easing of tensions and avoid escalatory actions, but cross-border attacks resumed almost immediately, with the Taliban reporting Pakistani mortar and rocket strikes wounding 45 people in Kunar province — described by Pakistani border forces as the most serious clash since the ceasefire was declared. The northern route is not merely complicated. It runs through an active war.

And even the traffic that does flow through Gwadar generates a revenue split that heavily favours COPHC: ninety-one cents of every transshipment dollar goes to the Chinese port operator, leaving Pakistan with nine. Pakistan’s traffic surge is real, but it is flowing through a bottleneck that the country lacks the financial resources and, so far, the institutional momentum to remove — and the revenue it generates is largely captured by someone else.

Until the depth problem is solved in a way that is fiscally sustainable over the long haul, and until the security, connectivity, and governance dimensions are addressed alongside it, Gwadar will remain a port that punches well below the weight of its geography.

{kind=link}